Let's get right to it: what exactly is corporate tax in the UAE? For years, the country was famous for its tax-free environment, but that's changed. The UAE now has a federal tax on business profits, a major shift for anyone operating here.

The standard rate is a very competitive 9%. But here’s the key part for small businesses: the first AED 375,000 of your profit is taxed at 0%. Think of it as a safety net, designed to give startups and SMEs the breathing room they need to grow.

Understanding the New UAE Corporate Tax Landscape

For decades, "UAE" and "zero-tax" went hand-in-hand, making it a hotspot for international entrepreneurs. The introduction of a federal corporate tax is easily the biggest shake-up to that model, bringing the nation’s financial rules more in line with global standards.

But this isn't a move to slow down business. It's more like the UAE is upgrading its financial operating system. The goal is to boost transparency, push back against questionable tax practices, and cement its reputation as a mature, sustainable, and trusted place to do business. This change actually strengthens its position as a top-tier global hub.

How the Tax is Structured

The system was built to be straightforward and supportive, especially for smaller companies. It’s a simple two-tier model that’s easy to get your head around:

- 0% Tax Rate: This applies to all your taxable profits up to AED 375,000. It's a deliberate policy to make sure startups and small businesses aren't held back by tax bills during their most critical growth phases.

- 9% Tax Rate: This is the headline rate, but it only kicks in for taxable profits above the AED 375,000 mark. Even at 9%, it’s still one of the most competitive rates you’ll find anywhere in the world, keeping the UAE attractive for larger corporations and foreign investment.

Here's a quick summary to keep things clear:

UAE Corporate Tax At a Glance

The table below breaks down the essential elements of the new federal corporate tax system, offering a snapshot for quick reference.

| Feature | Details |

|---|---|

| Standard Rate | A competitive 9% on taxable income. |

| 0% Rate Threshold | The first AED 375,000 of taxable income is taxed at 0%. |

| Effective Date | Applied to financial years starting on or after 1 June 2023. |

| Governing Law | Federal Decree-Law No. 47 of 2022. |

| Who It Applies To | All businesses and individuals conducting business activities under a commercial licence. |

This framework shows a clear commitment to supporting the business community while meeting international obligations.

This new regime was officially rolled out under Federal Decree‑Law No. 47 of 2022 and became effective for financial years starting on or after 1 June 2023. The law clearly sets the 9% rate for profits over the AED 375,000 (roughly USD 102,000) threshold, while locking in that 0% protected zone for smaller business profits. It's worth taking some time to learn more about the legislative trends behind this system and how it's being implemented.

The introduction of corporate tax is a strategic evolution, not a revolution. It balances the need for government revenue and international compliance with a continued focus on fostering a pro-business ecosystem that supports entrepreneurs and SMEs.

This fundamental shift means every business in the UAE—whether you’re on the mainland or in a free zone—needs to take a fresh look at its financial strategy and compliance. While it does add new responsibilities, the thoughtful, low-rate structure ensures the change is manageable. The core UAE tax benefits for international entrepreneurs are still very much alive and well. Getting a handle on this framework is your first step to navigating the new rules with confidence and setting yourself up for continued success.

Who Is Required to Pay Corporate Tax?

So, you understand the basics of the UAE’s new corporate tax, but the big question is: does it actually apply to your business? Let's break it down.

The law identifies who is a "Taxable Person", and this definition casts a pretty wide net, covering most businesses operating in the country. Essentially, if you hold a commercial licence to conduct business activities—whether you're an individual or a company—you're likely on the hook.

For businesses set up and registered in the UAE, the rules are straightforward. Whether you're running a business in Dubai mainland, Sharjah, Abu Dhabi, or even a Free Zone, your company is considered a resident for tax purposes. This puts you squarely within the scope of the new tax regime.

The system is designed to be fair, especially for smaller businesses. It features a statutory threshold where taxable income up to AED 375,000 is taxed at 0%. Only the profit above that amount is taxed at 9%. This provides built-in relief for startups and SMEs with modest profits.

Permanent Establishment for Foreign Companies

What about foreign companies? The rules extend to them, too, if they have a significant economic presence here. This is determined through a concept called "Permanent Establishment". Think of it as a test to see if a foreign company is just selling to the UAE or is actively operating from within the UAE.

A foreign company is typically seen as having a permanent establishment if it meets one of these two conditions:

- Fixed Place of Business: This is the clearest test. If your company has a physical, fixed location in the UAE—like an office, branch, factory, or workshop—it has a permanent establishment.

- Dependent Agent: This one is a bit more subtle. It applies if you have someone in the UAE who has the authority to regularly finalise contracts on behalf of your foreign company. For example, if you have a sales director based in Dubai who closes deals with local clients, their presence creates a taxable establishment for your business.

The distinction is crucial. A company that simply exports its goods to a UAE distributor, without having its own office or staff on the ground, would usually not have a permanent establishment. But if that same company opens a sales office in Dubai to actively market and sell its products, it crosses the line and becomes liable for corporate tax.

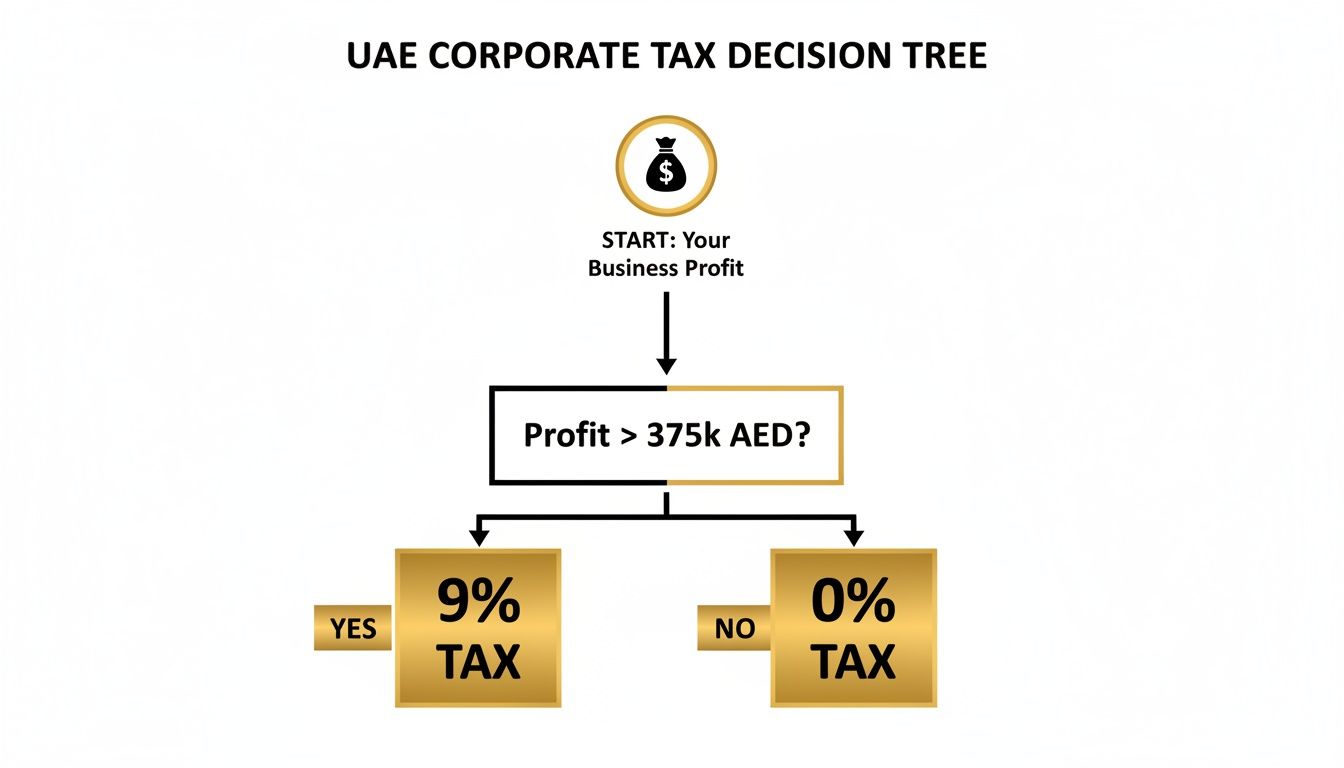

This decision tree shows at a glance whether the 9% corporate tax rate will apply based on your business profit.

As the infographic clearly shows, the system has two tiers, confirming that only profits that exceed the AED 375,000 threshold are subject to the 9% tax.

Individuals and Personal Income

One of the most common points of confusion is how this tax impacts individuals. Here’s the key takeaway: UAE corporate tax targets business profits, not your personal income.

This means your salary from employment, income from personal real estate investments, or dividends you receive from stocks are generally not subject to corporate tax.

The core focus of the Corporate Tax Law is on income derived from a business or commercial activity. Personal wealth and employment income remain outside its scope, preserving the UAE's attractiveness for individuals.

However, the line gets a bit blurry when an individual holds a commercial or trade licence. If you're a freelancer, sole proprietor, or an entrepreneur operating under your own name with a business licence, the profits you generate from that commercial activity are considered taxable. In that case, the same rules for calculating and paying tax apply to you just as they would to a larger corporation.

Ultimately, if your income is tied to a licensed business activity, you are considered a taxable person.

How Corporate Tax Works in UAE Free Zones

The UAE’s Free Zones have long been the crown jewels for international entrepreneurs, celebrated for their unique operational and financial perks. With corporate tax now in the picture, a new layer of complexity has been added. It's time to bust the old myth: being in a Free Zone no longer means you're automatically tax-free.

Instead, the new law introduces a special status known as a ‘Qualifying Free Zone Person’ (QFZP). Think of this as the key to unlocking the highly sought-after 0% corporate tax rate, but it comes with a strict set of rules you must follow to the letter.

Becoming a Qualifying Free Zone Person

Gaining QFZP status is like getting a VIP pass to an exclusive club. It grants you some incredible benefits, but only if you play by the club’s rules. To earn this status, your Free Zone company must meet several conditions laid out by the Federal Tax Authority (FTA).

Here’s what’s non-negotiable:

- Maintain Adequate Substance: Your business needs a real, physical presence in the Free Zone. This isn’t about just having a PO box; it means having an office, staff, and the right assets for your operations. A "paper" company simply won't cut it.

- Derive Qualifying Income: The 0% rate only applies to specific types of income, which we’ll get into next.

- Audited Financial Statements: You must prepare and maintain audited financial statements. This is all about transparency and proving your compliance.

- Not Electing to be Taxed: A QFZP must not voluntarily choose to be subject to the standard 9% corporate tax rate, a strategic choice that might only make sense in very rare situations.

Meeting these conditions is mandatory. The government’s goal is to ensure these tax advantages go to businesses that are genuinely contributing to the UAE's economy.

Distinguishing Qualifying Income From Taxable Income

Once you've secured QFZP status, the next crucial step is understanding which of your profits get that sweet 0% rate. The law draws a clear line in the sand between 'Qualifying Income' (taxed at 0%) and everything else (taxed at the standard 9%).

So, what exactly is Qualifying Income? Broadly speaking, it covers:

- Income from deals with other businesses located in any UAE Free Zone.

- Income from transactions with businesses located outside the UAE.

- Income from certain ‘Qualifying Activities’ like manufacturing, logistics, and fund management, even if your customer is on the mainland.

However, income from most transactions with your UAE mainland-based customers is typically taxed at 9%. This rule is in place to prevent Free Zone companies from having an unfair tax advantage over mainland competitors in the local market.

Key Takeaway: For a Qualifying Free Zone Person, income from selling to a company in another Dubai Free Zone is taxed at 0%, but income from selling to a customer on the Dubai mainland is generally taxed at 9%.

This dual-rate system means your bookkeeping has to be impeccable. You must be able to clearly separate your different income streams to apply the correct tax rates. If you need help structuring your operations correctly from day one, understanding the fine print of a Dubai Free Zone business setup is the perfect place to start.

To make this clearer, let's look at a side-by-side comparison of how tax is treated for a standard mainland company versus a QFZP. This really highlights why achieving this status is so valuable for businesses with international or inter-Free Zone operations.

Mainland Company vs Qualifying Free Zone Person Tax Treatment

| Aspect | Mainland Company | Qualifying Free Zone Person (QFZP) |

|---|---|---|

| Tax on Profits up to AED 375,000 | 0% | 0% |

| Tax on Profits above AED 375,000 | 9% on all taxable income. | 0% on 'Qualifying Income'. |

| Tax on Mainland-Sourced Income | 9% (above the threshold). | 9% on most non-qualifying income. |

| Tax on International Income | 9% (above the threshold). | 0% on Qualifying Income. |

| Substance Requirements | Standard business operational needs. | Strict and mandatory to maintain status. |

| Compliance & Auditing | Standard FTA requirements. | Must maintain audited financial statements. |

As you can see, the tax efficiency a QFZP can achieve is significant. The catch? You have to carefully manage your income sources and maintain strict compliance with all the rules. The Free Zone advantage is still powerful, but it now demands a much more strategic and informed approach to how you structure your business and manage your finances.

How to Calculate Your Taxable Income

Knowing the rules is one thing, but figuring out what they mean for your business’s bottom line is what really counts. So, how do you get from your company’s financial statements to the actual tax you need to pay? Calculating your taxable income for UAE corporate tax isn’t about plucking a number out of thin air; it’s a process of careful adjustment.

The whole journey starts with your accounting net profit—that final figure on your profit and loss statement. Think of this as your raw material. From here, you’ll make a series of specific tweaks to bring that number in line with the UAE’s tax law.

It’s like filtering your profit through a special tax lens. This involves adding back certain expenses that aren’t allowed and subtracting income that’s exempt from tax.

Identifying Exempt Income

First things first: not every dirham your business earns is going to be taxed. The UAE Corporate Tax Law carves out certain types of income as exempt, mainly to prevent double taxation and to keep the UAE an attractive place for investment. This is a critical step because every bit of exempt income you identify directly lowers your taxable profit.

Here are the most common types you’ll encounter:

- Dividends and Capital Gains: Any profits you receive from a ‘Participating Interest’ in another company (whether here in the UAE or abroad) are generally exempt. This usually applies when you own 5% or more of that company’s shares for at least 12 months straight.

- Foreign Permanent Establishments: If your UAE business has a branch in another country and it’s already paying tax there, you can choose to exempt its profits from your UAE tax calculation.

- Income from Non-Resident Operations: Income that a non-resident earns from operating aircraft or ships in international transport is also exempt, provided certain conditions are met.

Getting this part right is your first big move in refining that profit figure.

Understanding Deductible Expenses

Once you’ve set aside your exempt income, it’s time to look at your expenses. The general rule of thumb is refreshingly simple: if an expense was incurred wholly and exclusively to generate your business’s taxable income, you can deduct it. This covers most of your everyday operational costs.

Think of things like:

- Salaries, wages, and staff benefits

- Office rent and utility bills

- Marketing and advertising campaigns

- Professional fees for your lawyers or accountants

- Interest on business loans (though some limits apply)

But, and it’s a big but, not all expenses are created equal. Some can only be partially deducted, or not at all. For example, any expenses for entertaining clients, customers, or suppliers are only 50% deductible. Things like fines, penalties, and donations to unapproved charities are generally not deductible at all.

Keeping meticulous records isn't just good business practice—it's a legal requirement. Every deductible expense you claim must be supported by invoices, receipts, and clear documentation to stand up to scrutiny from the Federal Tax Authority (FTA).

The Power of Carrying Forward Tax Losses

What happens if you have a tough year and end up with a loss? The UAE tax system has a built-in safety net to help businesses get back on their feet. You can carry your tax losses forward indefinitely and use them to offset profits in future years.

This means a loss in one year can directly shrink your tax bill in a later, more profitable year. There’s just one key condition: you can only offset losses against a maximum of 75% of the taxable income in any single future year. It’s a smart balance that lets your business recover while ensuring the government still collects some revenue.

This provision highlights why filing your taxes accurately every single year is so important, even if you don't owe anything. Properly documenting a loss today turns it into a valuable asset for tomorrow, giving you a strategic tool that transforms a difficult period into future tax savings. It’s another reason why solid bookkeeping and expert guidance are absolutely essential for every business in the UAE now.

Your Essential Tax Compliance Checklist

Knowing the rules of UAE corporate tax is one thing, but staying compliant is the part that truly matters. To navigate the requirements, you need a clear action plan. Think of this as your roadmap to meeting your obligations smoothly and, more importantly, avoiding any costly missteps right from the start.

It all begins with one non-negotiable step: registering your business for Corporate Tax. Every single business that falls within the law's scope must register with the Federal Tax Authority (FTA). This applies to everyone, regardless of your profit levels or even if you don't expect to pay a single dirham in tax.

Kicking Off Your Compliance Journey

Registering is like formally introducing your business to the tax system. It tells the FTA that you understand your duties and are getting your house in order. The FTA is the government body in charge of the whole system, and as businesses started preparing their first returns for periods beginning from June 2023, getting this first step right became a top priority.

Getting the registration done on time is your first big test. The process isn't overly complicated, but it demands careful attention to detail. For a full walkthrough, check out our guide on how to register for corporate tax in the UAE, which breaks everything down.

Key Deadlines and Filing Obligations

Once you're registered, your focus shifts to the ongoing work of compliance. This really boils down to two key dates: the end of your tax period and your filing deadline. Your tax period is simply your business's financial year.

The crucial deadline to burn into your memory is that your corporate tax return must be filed within nine months of your financial year-end.

So, if your company's financial year wraps up on 31 December 2024, your tax return and any payment owed must be with the FTA by 30 September 2025.

This nine-month window is your preparation time. Use it wisely to gather records, finalise your calculations, and ensure every detail on your return is accurate and fully supported by documentation. Procrastination is not a viable strategy here.

To back up your tax return, you'll need to keep detailed and accurate accounting records. These aren't just for your own books anymore; they are the official evidence for every number you report. This includes:

- Detailed financial statements (like your Profit & Loss and Balance Sheet)

- Records of all income, expenses, and transactions

- Invoices, receipts, and bank statements

- Fixed asset registers and payroll records

The High Cost of Non-Compliance

The FTA has put clear penalties in place to make sure businesses take this seriously. Simple mistakes or missed deadlines can become very expensive. These aren't just fines for failing to pay tax on time; they cover everything from late registration and late filing to not keeping proper records.

Understanding what's at stake is critical. The financial penalties can be significant, and repeated issues could lead to more intense scrutiny from the authorities. For a wider view on this, there are great resources that explain avoiding corporate tax penalties for late payment.

By using this checklist as your guide, you can build a solid compliance framework from day one. This will help you manage your responsibilities with confidence and keep your business on a smooth, penalty-free path.

Let PRO Deskk Guide You Through the UAE's New Tax System

The arrival of corporate tax in the UAE has opened up a new chapter for businesses, bringing both fresh opportunities and a fair few complexities. After diving into the specifics for mainland and free zone companies, it's clear that getting expert advice isn't just a good idea—it's pretty much essential. That's where we come in.

Think of PRO Deskk as your specialist partner, ready to help you navigate this new terrain.

- ✅ Specialists in Mainland Company Formation in Dubai, Sharjah, or Abu Dhabi

- ✅ Specialists in Freezone Company Formation across the UAE

- ✅ Specialists in Golden Visa on Property or Investor Visa

- ✅ Specialists in Corporate PRO Services and Attestation Services

- ✅ 24/7 Support Service – Always here when you need us

- ✅ Cost-Effective Business Setup Solutions tailored to your needs

- ✅ Help you enjoy UAE tax benefits for International Entrepreneurs

Don't let tax complexities slow you down. Partnering with a specialist ensures you stay fully compliant while taking advantage of all the strategic benefits the UAE offers. Your focus should be on your business, not on paperwork.

Our team takes the entire administrative burden off your shoulders, handling everything from FTA registration to ongoing compliance so you can focus on what you do best—running and growing your business. Let our experience be your advantage; you don't have to figure this all out alone.

📞 Call Us Now: +971-54-4710034

💬 WhatsApp Us Today for a Free Consultation

Frequently Asked Questions

Getting to grips with the new UAE corporate tax system naturally brings up a lot of questions. Here, we tackle some of the most common queries we hear from business owners every day.

Is My Salary Subject to UAE Corporate Tax?

No, it isn’t. If you’re an employee, your personal income like salary, bonuses, and other employment benefits are completely outside the scope of the UAE Corporate Tax. This new system is aimed squarely at business profits, not individual earnings from a job.

The same generally applies to personal income you might make from real estate investments, bank interest, or share dividends. As long as you aren't required to hold a commercial licence for these activities, this income won't be touched by corporate tax.

What Is Small Business Relief?

Think of Small Business Relief as a helping hand for startups and smaller enterprises. It’s a special provision that allows businesses to simplify their tax obligations significantly. If your business is resident in the UAE and your total revenue for a tax period is under the AED 3 million threshold, you can opt for this relief.

Once you elect for it and are approved, you’ll be treated as having no taxable income for that period, which means no tax to pay. It’s a powerful tool, separate from the standard 0% rate on the first AED 375,000 of profit. Just remember, you still need to register for corporate tax and actively choose to apply for the relief in your tax return.

Do I Still Need to File a Tax Return If My Business Made a Loss?

Yes, absolutely. Every business that falls under the corporate tax law must file a tax return for each period. This is a mandatory step, regardless of whether you made a profit, a loss, or broke even.

Don’t think of it as just paperwork. Filing a return that reports a loss is strategically important. It allows you to carry that loss forward and use it to offset taxable profits in future years. When your business starts turning a profit, this can make a real difference to your tax bill.

How Does Corporate Tax Affect the Oil and Gas Sector?

Companies working in the extraction of the UAE’s natural resources, such as oil and gas, play by a different set of rules. They are generally carved out from the main federal Corporate Tax law.

This doesn't give them a free pass, though. These businesses continue to be taxed at the emirate level under long-standing agreements. These specific tax regimes often involve much higher rates than the standard 9%, reflecting the unique and critical nature of the industry. For more general tax questions or to see how these topics are handled elsewhere, you can explore resources like these general tax FAQs.

Navigating the ins and outs of corporate tax can feel overwhelming, but you don't have to do it alone. At PRO Deskk, we specialise in helping businesses with Mainland and Free Zone company formation, visa processing, and corporate compliance, ensuring you’re set up for success from day one.

📞 Call Us Now: +971-54-4710034

💬 WhatsApp Us Today for a Free Consultation with PRO Deskk.